The worldwide humanoid robotic market moved nearer to large-scale commercialization in 2025, with installations reaching an estimated 16,000 models worldwide, in line with new information from Counterpoint Research.

China accounted for greater than 80 p.c of all humanoid robotic installations through the yr, underlining the nation’s dominant function in early deployments. Adoption was pushed primarily by use circumstances in logistics, manufacturing, automotive, analysis, and information assortment, the analysis agency mentioned.

Chinese language suppliers dominate early market

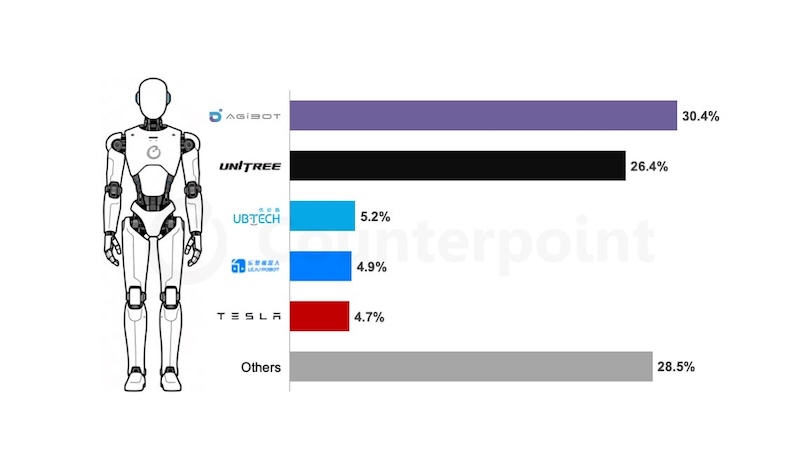

Shanghai-based startup AgiBot ranked first globally by annual installations in 2025, capturing round 31 p.c of the market.

The corporate started mass manufacturing of its X2 and G2 humanoid robots final yr and has deployed greater than 5,000 models from its Shanghai manufacturing facility throughout sectors together with hospitality, leisure, manufacturing, and logistics.

Unitree positioned second with a 27 p.c share, constructing on its background in quadruped robotics and movement management. The corporate has centered on growing lower-cost humanoid programs by producing key elements similar to motors, reducers, and sensors in-house.

UBTech ranked third with a share barely above 5 p.c. Its Walker-series humanoid robots are already getting used on automotive manufacturing facility flooring, with a deal with collaborative industrial duties.

Shenzhen-based Leju adopted intently, additionally capturing round 5 p.c of installations, supported by cloud-based coaching and software program upgrades developed in partnership with Huawei Cloud.

Tesla entered the highest 5 in 2025 with almost 5 p.c market share, pushed by elevated manufacturing of its Optimus Gen 2 and Gen 2.5 humanoid robots.

Counterpoint mentioned Tesla’s involvement has had a broader affect on the humanoid robotic provide chain, significantly in automotive manufacturing.

Collectively, the highest 5 humanoid robotic suppliers accounted for about 73 p.c of world installations in 2025.

From prototypes to scaled manufacturing

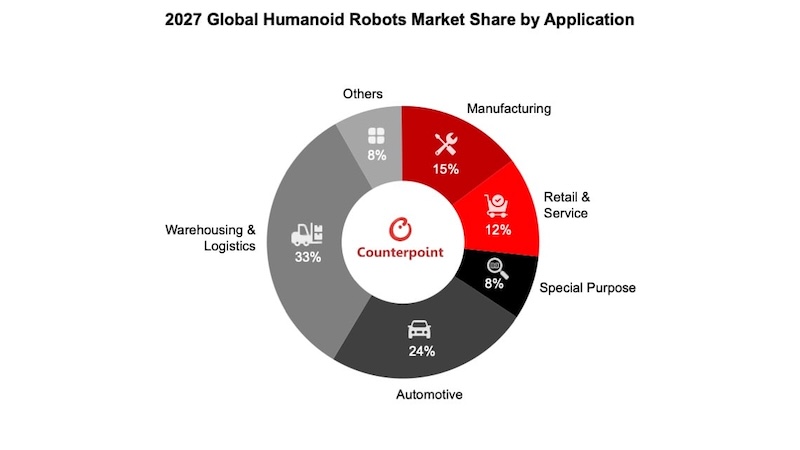

Counterpoint famous that 2025 marked a shift from experimental deployments towards early industrial rollouts, significantly in managed industrial environments. The analysis agency expects cumulative humanoid robotic installations to exceed 100,000 models by 2027.

By that time, logistics, manufacturing, and automotive functions are projected to signify about 72 p.c of annual humanoid robotic installations, reflecting the trade’s deal with structured, repeatable duties fairly than general-purpose shopper use.

Rising enterprise fashions and value stress

The report additionally highlighted a number of traits shaping the market’s subsequent section. Some Chinese language corporations are introducing lower-cost humanoid platforms geared toward interaction-focused use circumstances fairly than industrial duties, opening potential shopper and service-sector markets.

Robotic-as-a-service (RaaS) fashions are additionally gaining traction, significantly in China, the place corporations are providing humanoid robots for rental in areas similar to dwell performances, retail, and promotional occasions. Devoted platforms to handle leased robots are anticipated to emerge as deployments scale.

On the identical time, main suppliers are increasing manufacturing capability in an effort to cut back manufacturing prices.

Counterpoint pointed to aggressive automation plans by corporations together with Tesla and Determine AI, suggesting that humanoid robots might more and more be used within the manufacturing of different robots and industrial programs.

Whereas large-scale adoption stays a number of years away, the info means that humanoid robots are starting to maneuver past demonstrations and pilot tasks, with industrial use circumstances more likely to outline the market’s near-term development.